Getting started with FloatMe only takes a few minutes.

Sign up quickly using your phone. The process is simple and designed to get you up and running fast.

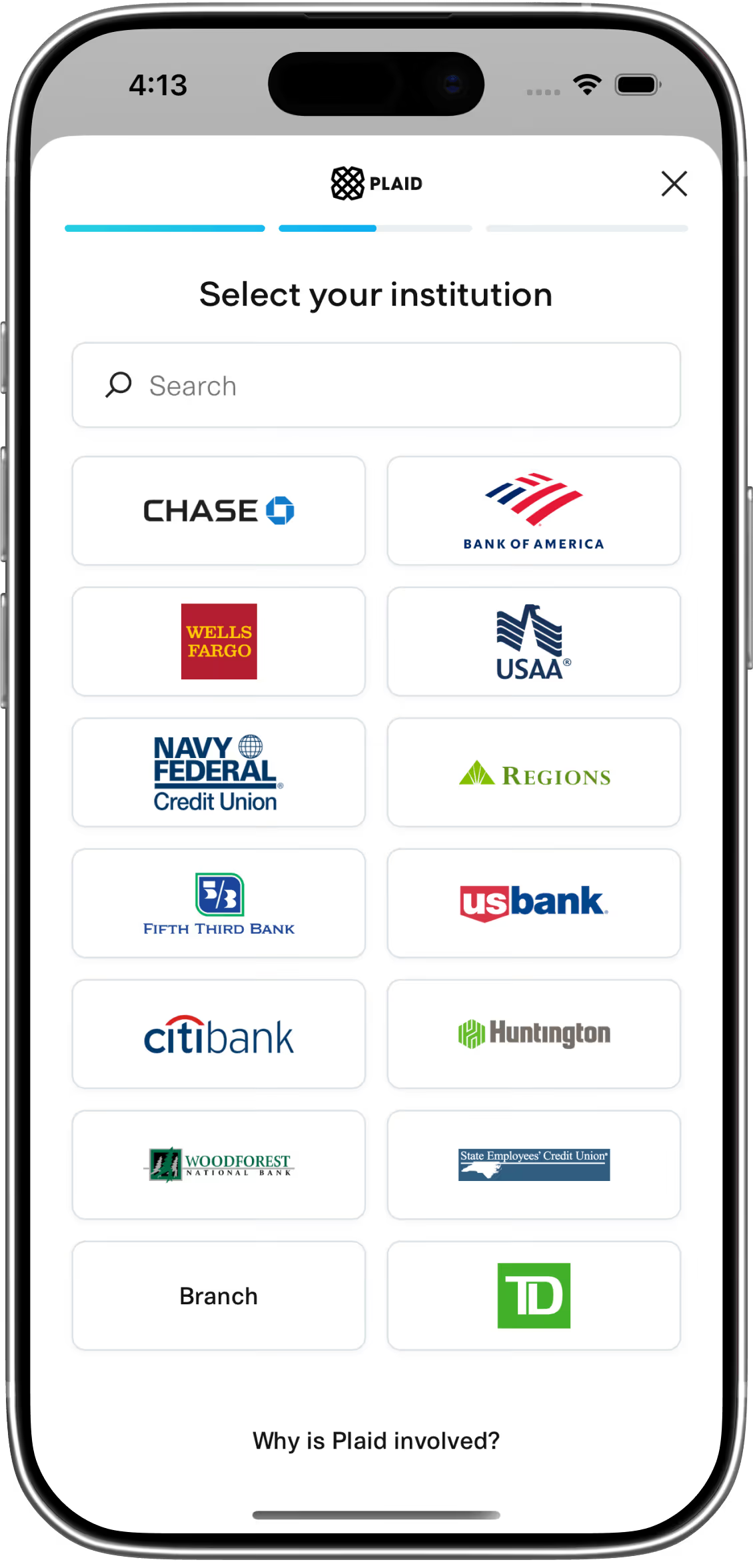

Securely connect your bank account so we can better understand your income patterns and determine eligibility.

FloatMe reviews your account activity, no credit check required. Once approved, you’ll be able to request a small advance.

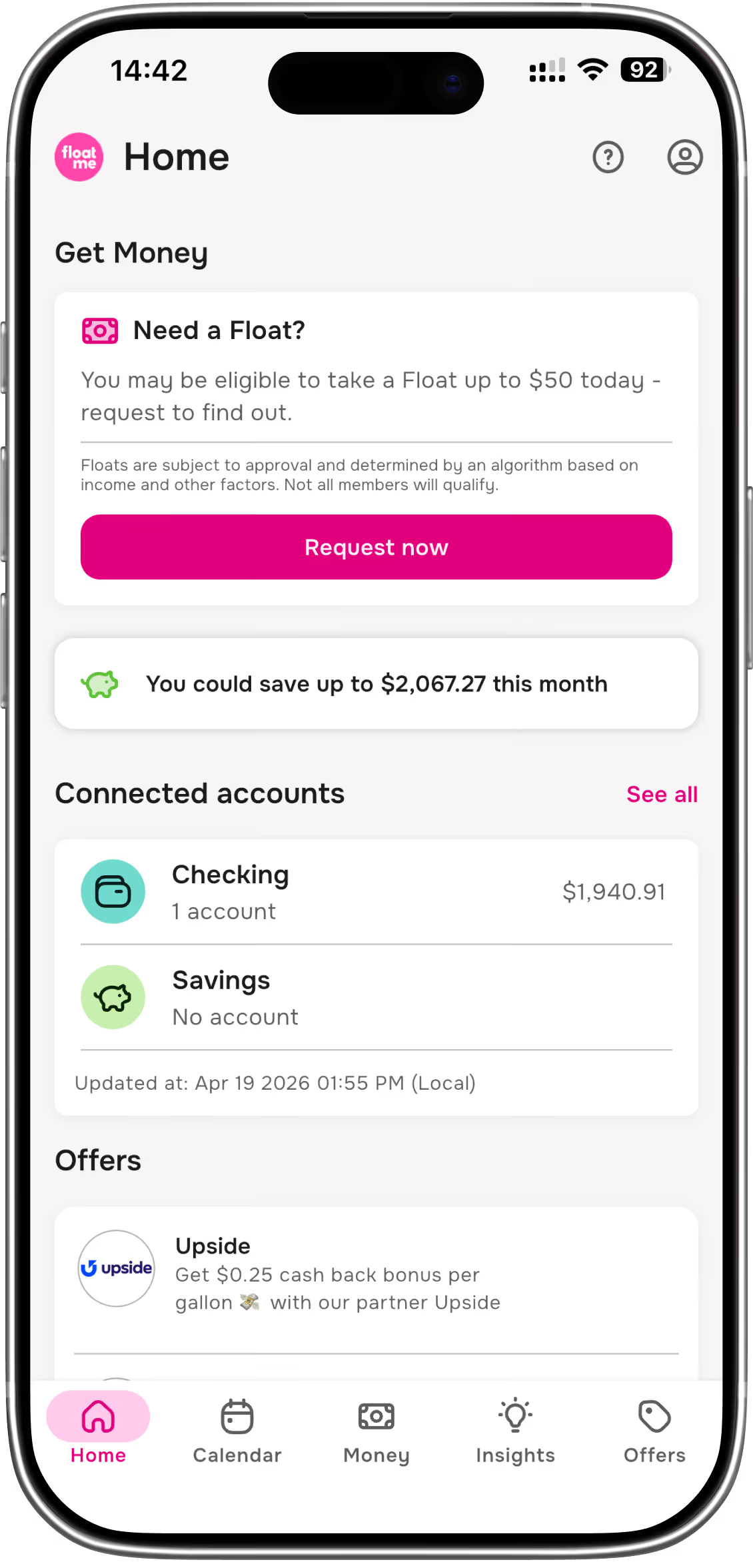

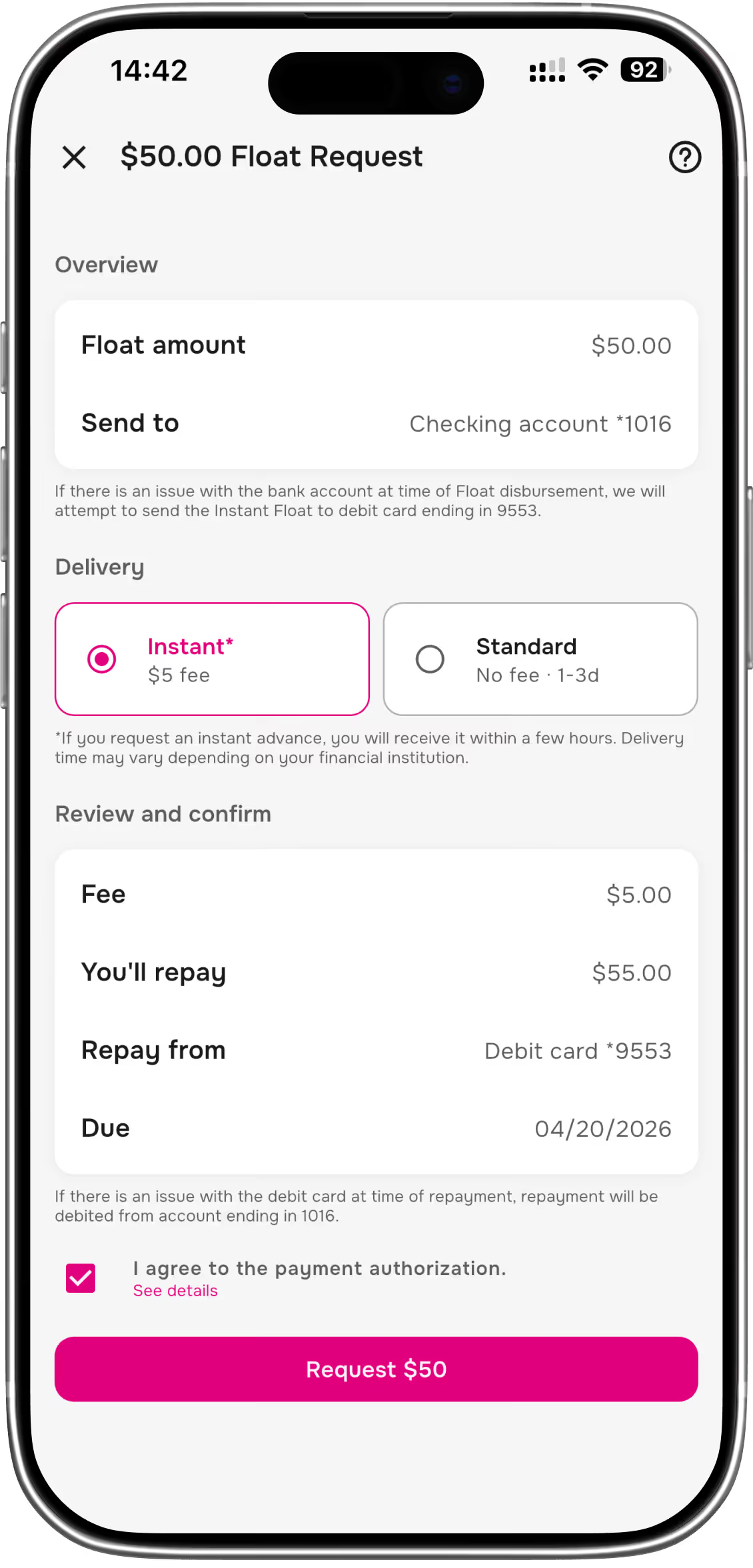

Choose a small amount that fits your needs (typically around $50) and request your float directly in the app.

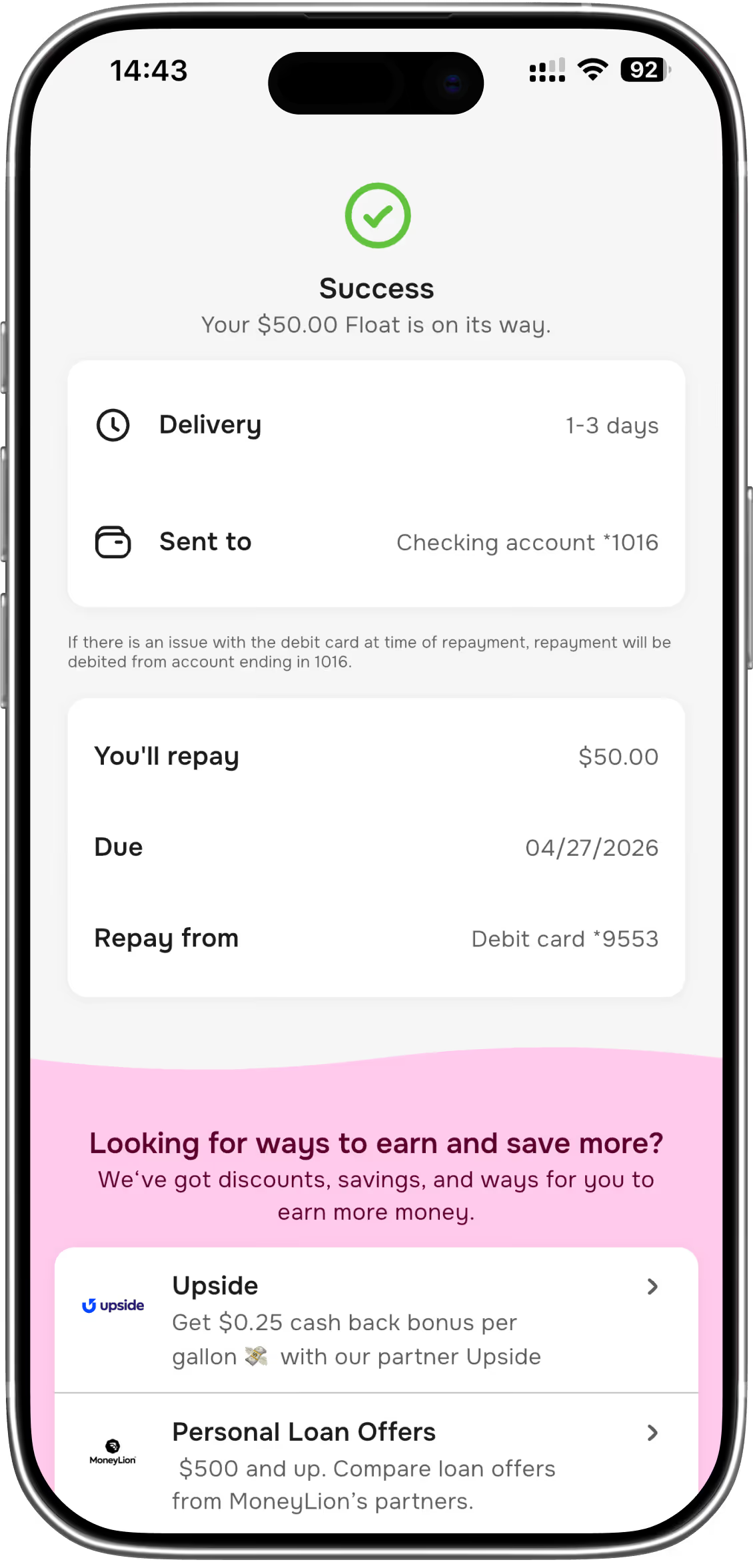

Funds are delivered as quickly as possible so you can take care of what matters. Timing may vary depending on your bank and transfer method.

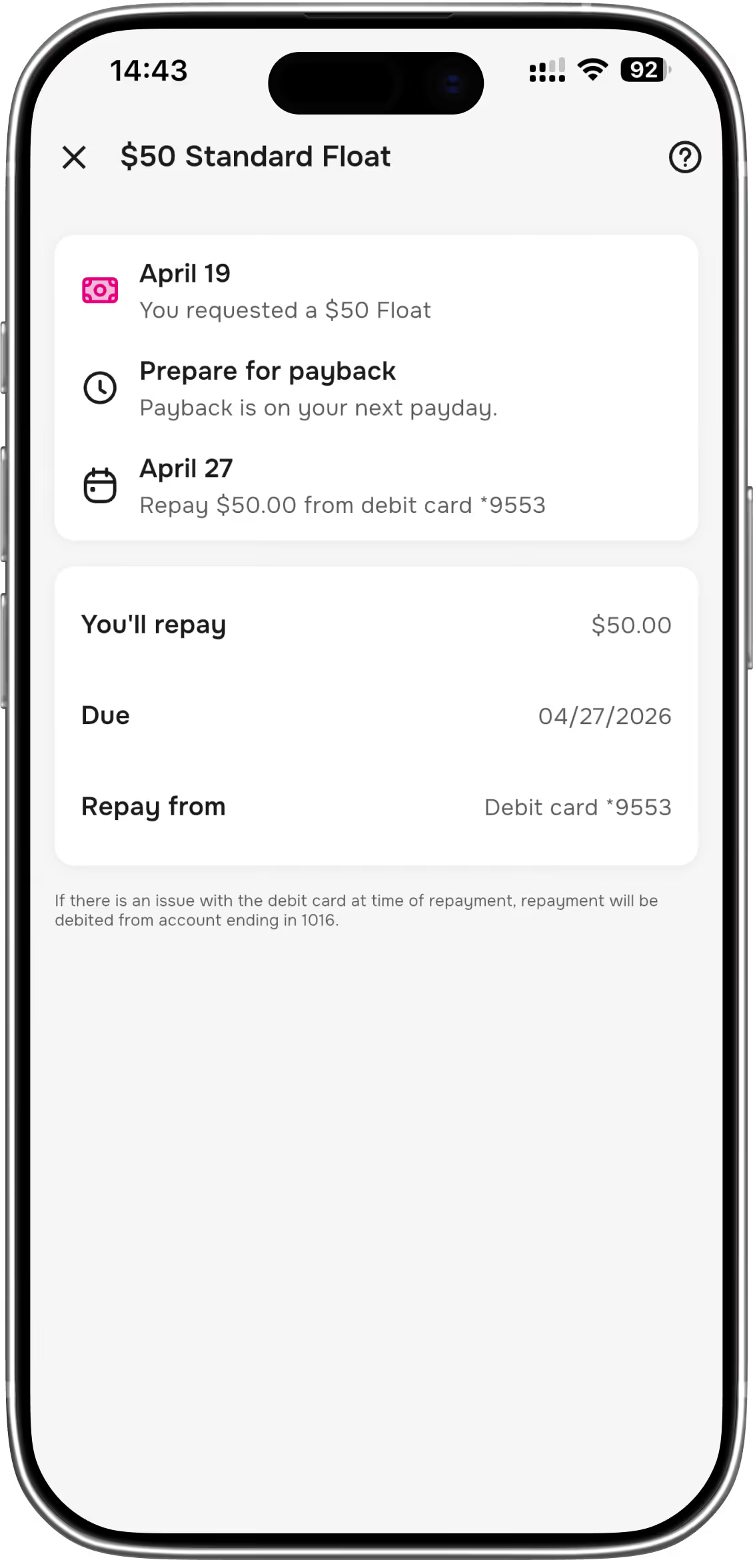

Your advance is repaid automatically when your next paycheck is deposited. No manual payments or complicated schedules. No interest, late fees or ba

FloatMe is designed for small, real-life expenses, Not large, high-risk loans.

Use it for:

There are a lot of cash advance apps out there. FloatMe is designed to keep things simple—and more manageable.

FloatMe isn’t a loan. It’s a tool to help you handle short-term needs without the risks that come with high-interest borrowing.

You stay in control, with a solution designed to support — not overwhelm — your finances.

Standard transfers typically arrive within 1 to 3 business days.

Need it sooner? Instant Floats can hit your account in as little as a few hours, depending on your bank.

No. FloatMe does not rely on traditional credit checks.

FloatMe focuses on small, manageable amounts up to $100.

Your Float is automatically repaid when your next paycheck hits, so there is nothing to keep track of.

Get the support you need to cover everyday expenses, without the stress and stay ahead of your next paycheck.